Author: Robert Osborne | X | LinkedIn

A View From The Top

- Crypto Market Trends Dictate Fundraising Cycles: Bitcoin ETFs, new all-time highs, and meme coin booms fuelled market optimism early in 2024, driving a 51% increase in Web3 venture funding from 2023. However, post-halving, market volatility tempered investment momentum, reinforcing the tight link between liquidity cycles and Web3 fundraising.

- Fundraising Rebounded but Fell Short of 2022 Levels: $19.6bn was disclosed across 3,516 Web3 deals, with an estimated total of $30bn raised including undisclosed rounds. H1 saw more deals (57% of the total), but H2 captured 61% of capital, indicating larger late-year rounds despite fewer transactions.

- Seed & Pre-Seed Thrived, Series A Lagged: Investors shifted capital towards early-stage projects, with median pre-seed and seed round sizes increasing. Meanwhile, Series A funding weakened, reflecting risk aversion and the rise of token-based fundraising alternatives.

- Category Winners: Mining, Compute & AI-Adjacent Projects: Mining & Validation median round sizes surged from $14.2m (2023) to $37.1m (2024), likely driven by post-halving dynamics. Compute Networks and AI-infused Web3 startups also saw strong investment, while gaming, metaverse, and advisory services struggled.

- Public Token Sales Dominated, Private Token Raises Lagged: Token fundraising grew 47% YoY, hitting $1.4bn, with public token sales accounting for 83% of deals and 61% of capital raised. A single $250m Avalanche sale skewed private fundraising totals, masking an otherwise weak performance.

- Regulatory Clarity Boosted Confidence Outside the US: Europe’s MiCA framework and other global regulatory developments provided stability, while US enforcement actions created uncertainty. Institutional interest rose, but cautious optimism persisted, with investors prioritising infrastructure and liquid token sales over speculative Web3 bets.

Web3 Fundraising Market Overview

In 2024, crypto markets experienced mixed performance. While Bitcoin reached new all-time highs following the January BTC ETF approval, the broader market struggled post-halving (see also Bitcoin Halving. The Four Year Cycle Is Dead). Market volume increased substantially early in the year, driven by institutional inflows. Meme coins and altcoins saw heightened volatility, with short-lived surges followed by sharp declines. Overall, the market’s maturity was evident as macroeconomic factors and demand-driven catalysts (like the ETF) increasingly outweighed traditional events like the BTC halving in influencing price action.

There is a close interdependence between crypto market performance and Web3 startup fundraising, rooted in both liquidity and sentiment. We looked at over 3,500 deals across all stages of Web3 fundraising in 2024 (see Fig. 1). The 2024 venture capital market invested in the blockchain technology stack saw a marked improvement from the previous year. There was a 35% higher deal count and a 51% increase in the capital fundraised from 2023 to 2024. Due to the wider crypto market conditions, however, the 2024 Web3 venture market failed to match the levels of activity and investment in 2022 (see Figure 1).

Figure 1: Web3 Deal Count and Capital Fundraised by Quarter, 2022-2024. Source: Outlier Ventures, Messari.

Broadly, when crypto asset prices rise, investors tend to have greater risk tolerance and more capital at their disposal. Often these are profits recycled into the venture capital market from realised token investments (see the section Token raises below). Many Web3 projects issue tokens for revenue generation, governance, and user incentivisation. Higher demand for these digital assets during more bullish crypto markets translates into increased liquidity. The effect of this is a positive feedback loop in which such startups attract more capital from both retail and institutional investors. Conversely, when crypto prices fall, caution sets in, reducing funding volumes and dampening valuations. Tokens (particularly compared to equity) become less attractive, diminishing Web3 projects’ ability to self-fund or attract investment.

In the context of the wider market experiencing mixed performance, something similar can be said more the Web3 fundraising market. In the first half of 2024, there were almost 2,000 fundraising deals across all stages, representing 57% of the deals in the whole year, with $7.7bn fundraised. The second half of the year, on the other hand, saw a reverse play. About 1,500 fundraising deals captured almost $12bn, almost 61% of the capital fundraised in the year (see Figure 2).

As mentioned briefly earlier, the approval of crypto-focused ETFs, new all-time highs for BTC, renewed interest from retail investors in the meme and alt coins markets have all contributed to a more supportive environment for Web3 investments. Whilst the SEC in the United States pursued a hard stance against crypto, regularity clarity elsewhere in the world (such as in Europe with the MiCA framework) gave investors a certain level of assurance.

Additionally, there has been a recovery of positive sentiment following the 2022 disasters (principally Terra-Luna in May 2022 and FTX in November 2022). New capital steered clear of the Web3 venture capital market, meaning the majority of startup investment came from the large reserve of dry powder that had been shored up in 2021 and 2022 (see Fig. 3). The hangover is still lingering in the Web3 venture capital market but a cautious optimism is returning, as indicated by a number of high-value deals: Avalanche ($250m private token sale), Berachain ($100m Series B), Eigen labs ($100m Series B) Farcaster ($150m Series A), Monad Labs ($225m Pre-Series A), amongst others, underscore a fundamental confidence from investors in the promise of blockchain technology.

Below we examine different areas of the market to achieve a more comprehensive view of Web3 fundraising developments in 2024.

Round Sizes and Deal Count by Stage

How then has Web3 venture capital fared in the context of the wider market that has had mixed performance? Looking at round sizes and deal count across different stages, here are the key takeaways:

- Seed stage rounds saw the most capital fundraised, representing 14% of the capital fundraised and 16% of the deal count across all stages (see Figure 4).

- Accelerators funded the long tail of Web3 projects, accounting for 25% of all fundraises and 48% of early stage startup fundraises (accelerator to Series A).

- We’ve seen average round sizes for the following stages (see Figure 6):

- Pre-seed: $2.5m, an increase of 28% from 2023 (almost $2m round size).

- Seed: $5.6m, up from $5m the previous year.

- Series A: $17.6m, down from $18.1m in 2023.

Our focus is on the Web3 fundraising venture capital market in this overview is on early stage deals. Later stage rounds (Series B+, strategic rounds, treasury diversification and debt financing) primarily track the survival of established startups, making them less interesting for understanding market shifts, new company formation, and investor sentiment. By contrast, pre-seed, seed, and Series A fundraises are key stages to look at in more detail because they provide early indicators of investment trends, risk appetite, and liquidity conditions.

It should be noted that the data for capital fundraised in Figure 4 is less than the total amount fundraised in Web3 venture capital. This is because it is quite common for projects not to disclose how much they fundraised. For example, in 2024 there were 3,516 fundraised deals across all stages but only 2,268 disclosed how much capital was raised (65% of the total). The proportion of ‘disclosed’ varies stage by stage. For example, 75% of pre-seed deals disclosed capital fundraised, 85% for seed stage and 91% for Series A. Figure 5 illustrates this further with estimations of the total capital fundraised in these three stages.

For early stage deals, we can estimate that there was 15% more capital fundraised than what is published publicly, bringing the total estimated capital fundraised by pre-seed, seed and Series A projects to nearer $6.6bn in 2024. Extrapolating this to encompass all stages, a cautious estimate of $30bn was fundraised by Web3 projects in 2024 (versus $19.6bn disclosed capital fundraised).

Companies may choose to keep their fundraising amounts undisclosed for several strategic reasons, including competitive secrecy, investor privacy, and negotiation leverage. Startups in stealth mode or those operating in highly competitive sectors may not want to reveal their capital reserves to avoid signaling their runway or valuation to competitors. Some investors, particularly family offices or strategic backers, may also prefer privacy. Additionally, underwhelming fundraising outcomes (raising less than expected) could lead to negative perceptions from future investors. The increase in disclosure rates from pre-seed to Series A reflect growing market validation in the company. As companies mature, they are more likely to publicise successful raises to attract talent, customers, and future investors. Pre-seed startups, still validating their ideas, may be more cautious, whereas Series A startups often see disclosure as a way to signal strength and momentum.

Examining median round sizes of different stages is also useful when identifying typical funding dynamics. Total capital fundraised can be skewed by a few massive rounds, making it harder to assess whether funding conditions are improving or deteriorating for the average startup. Similarly, deal count alone doesn’t reveal whether startups are raising larger or smaller rounds on average. A high deal count could still coincide with declining round sizes if funding is becoming more fragmented. Median round size can shed light on funding trends, founder leverage, and investor risk appetite, offering a more interesting proxy of market activity.

Pre-seed and seed stage rounds ended the year with higher median round sizes than when they began in January 2024. The positive trend was stronger for the pre-seed stage, which reached their smallest median round size in July after which it experienced a fairly consistent upward trend. Series A, however, did not fare so well, with the median round size in December 2024 being less than half of what it started at in January.

Series A Web3 fundraising struggled in 2024 due to increased risk aversion among investors, shifting macro conditions, and a preference for earlier-stage bets with higher upside potential. While institutional interest in crypto grew following Bitcoin ETF approvals, broader market uncertainty (driven by regulatory challenges, liquidity fluctuations, and volatile token markets) made later-stage investments less attractive. Many Series A startups faced difficulties proving sustainable traction in a market still recovering from previous cycles, leading investors to shift capital towards pre-seed and seed-stage projects where valuations were lower, and potential returns were higher. Additionally, the rise of public token sales and renewed enthusiasm for new narratives (e.g., DePIN, AI + crypto) incentivised backing earlier projects with fresh go-to-market strategies rather than doubling down on Series A startups struggling to scale.

Category Differentiation

Web3 is a shorthand for projects building on the blockchain technology stack. In reality, different categories within this scope have different capital requirements and are subject to their own trends of popularity amongst developers and investors alike. In Figures 7 and 8, the average round size is measured against the average stages at which each Web3 category fundraises. In this way, a proxy for the relative maturity and capital requirements of each category is generated.

In 2023, fewer early stage projects were able to fundraise, which shifted many categories along the axis towards relatively greater stage maturity. Cross-Chain Interoperability ($26.9m) and Mining and Validation ($14.2m) saw the largest median round sizes, reflecting continued investor interest in foundational infrastructure for blockchain scalability and security. Conversely, categories like HR and Community Tools ($1.46m) attracted significantly less capital, indicating lower demand for these solutions. Financial Services ($5.85m) and Compute Networks ($6.19m) also saw moderate funding, aligning with broader trends in Web3 infrastructure development.

By 2024, Mining and Validation ($37.1m) saw a massive surge in funding, likely due to the post-Bitcoin halving recalibration and growing institutional interest in crypto mining amid regulatory shifts. Compute Networks ($14.38m) also experienced significant growth, possibly driven by AI and DePIN-related investment trends. Meanwhile, Cross-Chain Interoperability funding plummeted to $2.3m median round size, suggesting a reduced appetite for bridge-related projects following security concerns and an industry pivot towards native multi-chain solutions. The decline in Consultancy and Advisory ($7.8m to $2.3m) and Metaverse and Gaming ($2.85m to $1.74m) suggests investor focus shifted away from speculative narratives towards more utility-driven categories. The mixed performance across categories and a greater spread of maturity reflects the evolving priorities of Web3 investors, favouring infrastructure, AI-adjacent technologies, and mining over previously hyped sectors.

Token Raises

We looked at 638 token raises across 2024. Here are the key takeaways:

- $1.4 billion was raised across both private and public token sales in 2024. Overall, the first half of the year saw a stronger performance, accounting for 54% of the capital raised and 64% of the total private and public token sales (see Figure 9).

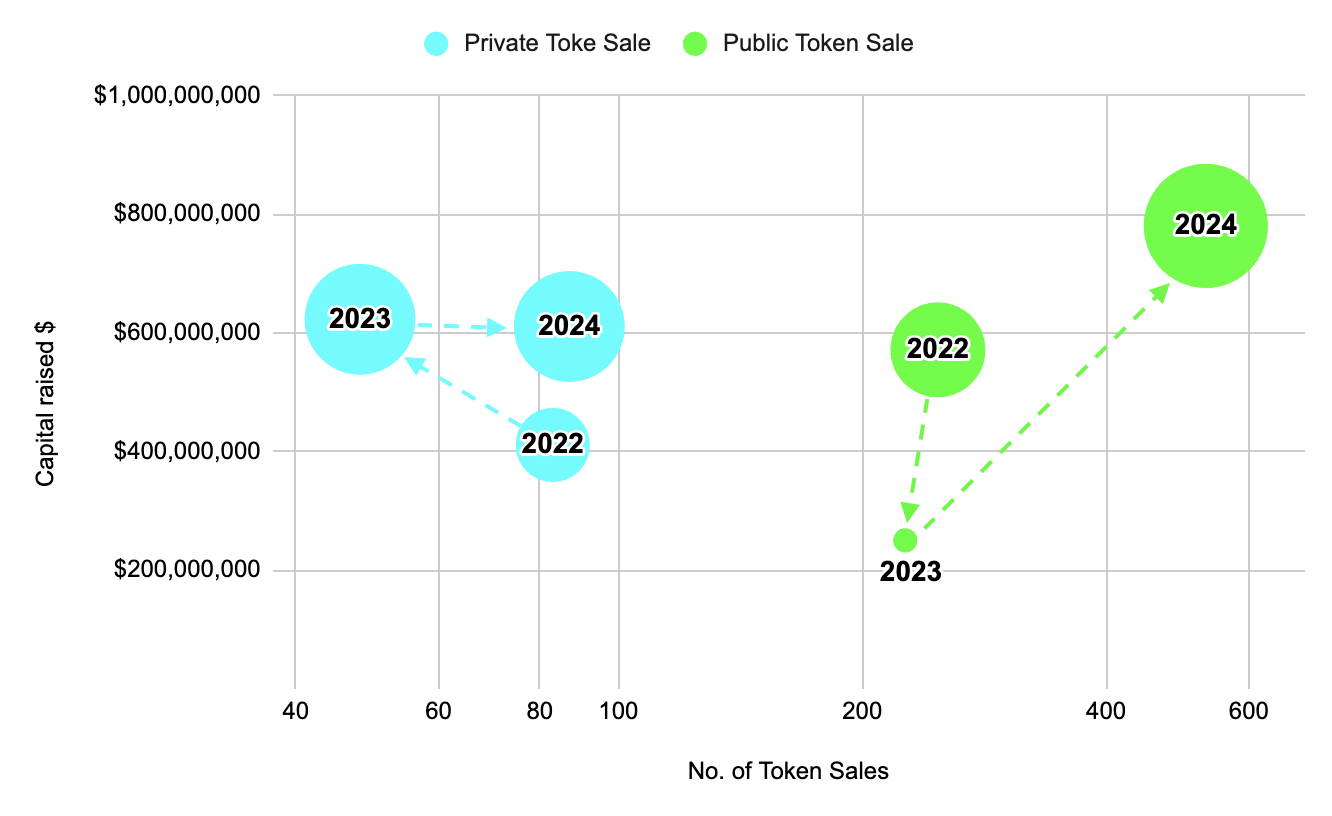

- Public token sales dominated token fundraising: public token sales accounted for 83% of all the sales events and 61% of the capital raised in 2024.

- There were more than double the number of total token raises than 2023 (274 private and public sales), and a 47% increase in capital raised (see Figure 10).

- A true Avalanche: the $250m private locked-token sale from Avalanche in December accounted for 49% of all the capital raised in 2024 private token sales.

The overall growth in token sales can be attributed to heightened institutional interest, regulatory advancements, and the approval of Bitcoin ETFs, which bolstered market confidence. However, the market also faced challenges, including increased volatility in meme coins and altcoins, which may have influenced investor sentiment and participation in token sales.

In the summer of 2024, private token sales experienced a notable downturn, with capital raised dropping from $26.3m in June to $7.2m in July and further to $3.3m in August. This decline coincided with broader market challenges, including significant sell-offs in Bitcoin and other cryptocurrencies. Factors such as government sales of seized Bitcoin, notably by Germany, and the initiation of Mt. Gox creditor repayments contributed to increased market volatility and investor caution. Additionally, weak economic data heightened recession fears, leading investors to retreat from riskier assets, including private token investments. These combined events eroded investor confidence, resulting in reduced participation in private token sales during this period.

In 2022, the crypto market faced significant challenges, including high-profile scandals and substantial price declines, leading to a cautious investment environment. Despite these hurdles, public token sales were more prevalent, with 248 deals raising approximately $571m, while private token sales comprised 83 deals totaling around $411m in 2022. The year 2023 marked a shift in investor strategy. Private token sales, though fewer in number with 48 deals, saw a notable increase in capital raised, reaching about $623m in 2023. Conversely, the same year saw public token sales decreased to 226 deals, raising approximately $250m. This 2023 trend suggests a growing investor preference for private sales, possibly due to increased due diligence and a focus on projects with perceived higher potential amidst market recovery efforts.

In 2024, private token sales stagnated whilst public token sales recovered and outperformed 2022 activity. With the exception of Avalanche, private token sales in 2024 performed poorly. If the AVAX sale is removed from the dataset, private token sales in 2024 raised 12% less in 2022. Public token sales, on the other hand, almost equaled both 2022 and 2023 combined (95% of the previous two years’ total) and saw 12% more total deals. The combination of improved liquidity, a strong Bitcoin rally, and a boom in meme coins and altcoins contributed to the surge in public token sales, making them the dominant once again.

Build Bigger. Build Better. Build with Us.

Outlier Ventures is always on the lookout for visionary founders ready to shape the future of Web3. Our Base Camp accelerators provides hands-on support from industry experts, access to a powerful network of partners and mentors, and the tools you need to scale. If you’re building the next breakthrough in blockchain, AI, or the open metaverse, we want to hear from you. Explore our open programs and apply today.