Uber, which we all may be familiar with, is a network for buying and selling car rides. The company that grows and maintains this network plays a vital role. For playing this part, this centralised entity is able to extract significant rent from the network.

Is that justified? Of course it is; the network wouldn’t be as popular as it is without the efforts and investment of this entity. What if there was a way to scale a network without this middleman extracting rent? Leaving more value to be captured by the network participants. Enter crypto-networks.

A primer on crypto-networks

At their core, crypto-economic networks are two sided marketplaces. Just like Uber. A Layer 1 for example is a marketplace for blockspace, a decentralised digital resource network (aka dePIN: Decentralised Physical Infrastructure Network) is a marketplace for resources such as compute or storage.

Two-sided marketplaces may also exist at the application layer – data unions are a marketplace for data, and DEXs are a marketplace for liquidity.

What is the difference between a one-sided marketplace and a two-sided one? The former is a market in which you can be either the consumer or the producer of value, but not both. An example would be AWS, in which you are either a consumer of computation and storage resources (consumer), or you are Amazon (producer). These different types of marketplaces are also referred to as ‘pipelines and platforms’.

In a two-sided marketplace, any participant may play either role. In a decentralized compute marketplace, anyone can permissionlessly join the network as a producer of value (node runner; compute provider) or a consumer of value (pays the nodes for access to compute).

Crypto allows us to create two-sided marketplaces much more easily for digital resources and allows them to exist in a decentralised (or more distributed) way. Doing so has shown that these marketplaces can achieve superior unit economics and that they can operate in censorship-resistant manner.

Crypto-networks are self-organising two-sided marketplaces with their own economic policies.

What are some everyday two-sided marketplaces?

eBay is quite an intuitive example – it is an online bazaar where anyone can list something for sale, and anyone else can buy it. It is two-sided because you can both list, and buy. Simultaneously even if you wanted to.

Youtube is another marketplace we use every day. Contributions of content can be made by anyone, and anyone else can consume this value. For providing this platform, Youtube takes a cut of course – it monetizes via selling this attention to those seeking adspace. Some of this revenue is shared with top creators, however it is not often significant enough to stop them from exploring other monetization avenues.

The difference between these marketplaces and crypto-networks is that a central party is needed to coordinate all the stakeholders in these networks. They play a vital role, and for that, they extract a big fee. Furthermore, history has shown that a monarch having absolute power is not always a good thing (although there are cases in which it is preferable!)

However, what if we had a way to coordinate actors without this monarch? This is what crypto has brought to the world. Crypto-networks align the incentives of disparate stakeholders such that they can all rally around national incentive: making more money.

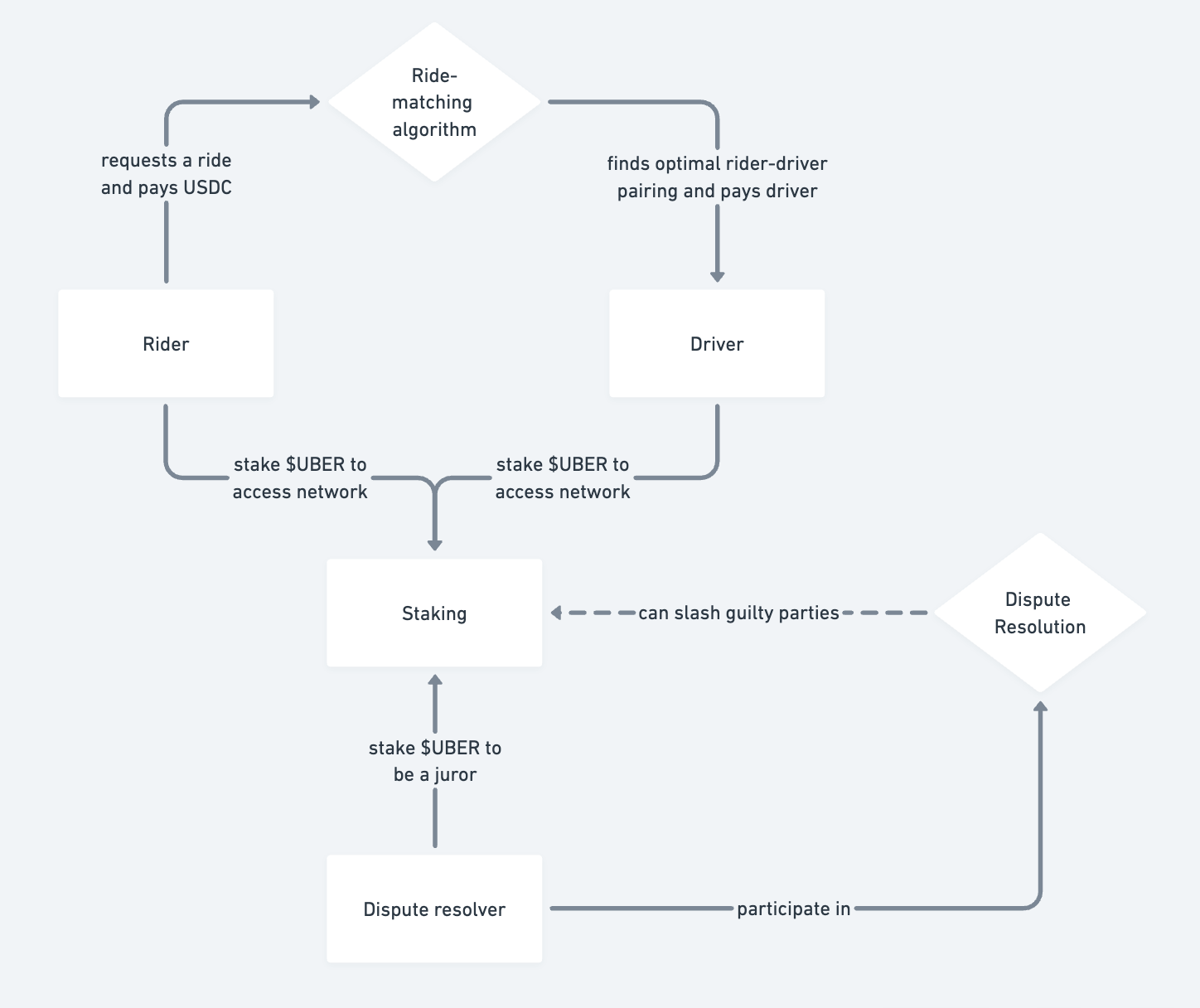

What would a crypto version of Uber look like?

This is a thought experiment to help us think through and understand how crypto-networks work from a high-level economics perspective, and how they align incentives without a central party calling all the shots – and extracting significant value from the network.

Firstly, let’s define the roles in the network:

- Drivers

- Riders

- Dispute settlers (when a driver and a rider enter a dispute; who is the arbiter of justice?)

Drivers

Now, how does one become a driver? Well one would need a car of course. After that, how can we make sure that they can be trusted to drive strangers around? What if they don’t have a driver’s license? What if their car is not fit for the road?

Usually, crypto-networks like to make the producer of value put up some money as collateral to ensure their good behaviour. In this example, a driver would have to stake some tokens, say 100 $UBER which can be slashed (confiscated) if they are found to be bad drivers.

How can we find them to be bad drivers though? Perhaps a sufficient mechanism here could be that more than 20% of their rides rate them 4 stars or below, or they receive 5 1 star reviews within 20 rides.

Slashing a stakeholder is much easier in a digital environment, as you can make interactions easily verifiable by others, whereas in the physical plane this is more challenging. For more on this, check out this article.

Riders

What of the riders? Anyone can become a rider. In order to ensure their own politeness and good behaviour, we can make them stake some $UBER as well. However we don’t need to make the threshold as high as it needs to be for a driver, as there is higher risk with onboarding a bad driver with a bad car.

When downloading the crypto-Uber app, riders must stake $10 UBER to start ordering rides, and pay in $USDC the full fare directly to the driver.

Since there is no middleman here to extract a large amount of rent – the revenue for drivers may be higher, or the fees for riders may be lower. Or both!

There is still one issue here; what happens when there is a dispute between a rider and driver? What happens when there is a case of ‘he said she said’ who settles these disputes?

Dispute Settlement

Dispute settlement mechanisms exist in all marketplaces, however they are a different matter if we want things to operate in a ‘decentralised’ way. If there is no centralised party to be the arbiter of truth – how can we incentivise network participants to play this role?

We can draw inspiration from the mechanism used by Kleros Court, in which a pool of token stakers are randomly selected from to be the jurors to settle a specific dispute.

Each juror receives the relevant information about the case, and makes a vote in favour of one of the parties. After all jurors have voted, the results are revealed. The winner of a dispute between a rider and driver is therefore the party that receives the majority of votes (there must be an odd number of jurors).

The jurors in the minority – the losing side – have their tokens slashed, and these confiscated tokens are awarded to the majority voters. This creates a mechanism in which jurors are incentivised to vote for what they believe the other jurors will vote for. This creates a schelling point where the dispute settlers can reach a subjective consensus.

After reaching a result, one of either the rider or the driver can be found guilty, and slashed accordingly, with the tokens being awarded to the offended party.

What about governance?

If there is no central party, who makes the decisions in the network? Who decides whether and how to tweak the matching algorithm? Or how many tokens must be staked to participate in the network? Or even the monetary policies of $UBER?

Why, the Uber DAO of course! How can it work?

Many DAOs operate on a ‘1 token = 1 vote’ system, however in practice this has not proven to be very useful, and just results in oligopolies most of the time. Instead, we can award governance to stakeholders that are active users of the network, as opposed to stakeholders that have a lot of money but are otherwise not very aligned.

One way of achieving this is by awarding certain ‘badges’ (NFTs) to power users. For example:

| Driver | Rider | Juror | Rank |

| Successfully completes <250 rides without serious incident | Successfully completes <750 rides without serious incident | Participates in >10 disputes successfully as a majority voter | 1: has a voting weight of ‘2 units’ in governance decisions |

| Successfully completes 250-1500 rides without serious incident | Successfully completes 750-2500 rides without serious incident | Participates in 10-50 disputes successfully as a majority voter | 2: has a voting weight of ‘5 units’ in governance decisions |

| Successfully completes 5000+ rides without serious incident | Successfully completes 2500+ rides without serious incident | Participates in 50+ disputes successfully as a majority voter | 1: has a voting weight of ‘15 units’ in governance decisions |

The numbers given above are arbitrary and in practice, finer criteria would have to be used. Please also note that one party may play multiple roles in the network! And simultaneously hold multiple badges, increasing their voting power (for example, a rider can also be a juror).

Furthermore, these credentials may also affect the ride-matching algorithm and discriminate in favour of trusted, reliable stakeholders.

Value Capture

As the crypto-uber app gets more downloads and onboards greater numbers of users, more and more people must buy and stake the token – taking it out of circulation. Therefore, the more the network grows at it achiever more and more success, the more the $UVER token captures value.

This achieves 2 main things:

- Incentivises people to join the network early if they believe it is solving a real problem and will grow in value

- Aligns the incentives of the participating stakeholders, and makes sure they act in positive-sum ways such that the value of the $UBER tokens grow and they do not lose them due to misbehaviour

Conclusion

The benefits here are mainly the greater value capture for network participants (assuming well engineered economics), and user ownership of the network.

However there are drawbacks as well:

- Worse UX since drivers/riders need to buy and stake tokens

- Liability to network participants of actually losing money via getting slashed

- Decentralisation can be a disadvantage, especially as the network is trying to scale

- Immature abstraction services for removing the complexity of dealing with these networks

This article is intended as a thought experiment to highlight what crypto networks are.

They are self-organising systems in which stakeholders do not have to know or trust each other to be aligned in their goals. To explore how this can work, we applied these crypto-economic principles to a two-sided marketplace like Uber, and theorised what it may look like if it were to operate in a decentralised fashion.