What fundraising instrument is right for my Web3 startup?

Introduction

Since 2014, Outlier Ventures has collaborated with and invested in over 250 Web3 startups through our Basecamp accelerator and Ascent token launch programs. During this period, we’ve encountered numerous Web3 companies seeking to raise from venture capital using various fundraising instruments. These companies span a wide spectrum, ranging from those that are exclusively equity companies and have no intention of ever launching a fungible token to those who are open to the idea of integrating a fungible token into their future plans but are uncertain about how it fits with their current product design. Lastly, there are companies looking to raise capital that require a token for their product or network to function correctly.

This blog post aims to outline the three major fundraising instruments, outline their key features, and provide a high-level guide to help you determine the most suitable investment contract for your Web3 startup.

SAFE

A SAFE or ‘Simple Agreement for Future Equity’ is a type of investment contract that is commonly used in early-stage startup fundraising. The SAFE fundraising contract was developed by Y Combinator in 2013 as an alternative to convertible debt and has become a very popular equity fundraising instrument.

In a nutshell, a SAFE is a convertible instrument that will give the investor the right to buy equity shares in the future, specifically, at the time the company will raise a priced round, such as a Series-A or an alternative contractually agreed liquidity event. A SAFE round is not priced and the documentation involved is rather simple overall. The project presents it to investors with a couple of clauses to negotiate, such as the amount of money invested by the investor and the terms of the conversion mechanism, whether that is a valuation cap or a discount. . This results in the SAFE investor sharing in the upside of the company between the time the SAFE is signed (and funding provided) and the trigger event.

Some key features of a SAFE include:

- Simplicity: SAFEs are typically simpler and shorter than traditional equity investment documents like convertible notes or preferred stock agreements. This makes them more accessible and less expensive to structure for early-stage startups, allowing them to get access to financing very quickly.

- Future equity: A SAFE will not allow the investor to get shares issued immediately. Instead, it represents a promise of future equity in the company. Investors provide money to the startup in exchange for the right to convert their investment into equity at a later date, typically when a specific triggering event occurs.

- Conversion trigger: SAFEs typically have a specified event that triggers the conversion of the investment into equity. This event is often the closing of a subsequent equity financing round (e.g., a Series-A funding round), the sale of the company, or some other predefined milestone.

- Valuation cap and discount: SAFEs may include a valuation cap and a discount to provide early investors with favorable terms when converting their investment into equity. The valuation cap ensures that early investors do not overpay for their equity, and the discount offers them a lower price per share compared to the price paid by later investors. The mechanism to be applied upon conversion will be the one that results in a greater number of shares for the investor.

- No interest or maturity date: Unlike convertible notes, SAFEs do not accrue interest, and typically they do not have a maturity date, which means they usually do not need to be repaid if the triggering event does not occur.

- Risk: SAFEs are considered riskier for investors than traditional equity investments, as they lack certain rights and protections typically associated with owning equity shares. In the event of a startup failure, SAFE holders’ rights are typically junior to and more limited when compared to those of preferred stockholders’ rights.

- Variations: There are various versions of SAFEs, and the specific terms can vary from one agreement to another. Startups and investors can negotiate the terms of SAFEs to some extent, but they are generally simpler and more standardized than traditional investment contracts.

SAFT

As SAFEs became one of the most popular methods for early stage equity fundraising, it was only logical that the crypto industry modified this widely used fundraising instrument to allow for raising capital via a promise of a future token. This led to the emergence of SAFTs or ‘Simple Agreement for Future Tokens’, also known as ‘TPSA’s (Token Pre-Sale Agreements). A SAFT is designed to simplify the fundraising process and create a framework for raising capital for pre-token blockchain startups.

If a blockchain startup knows their technology requires a token to function correctly, they can raise venture capital by selling investors an allocation of a token at some point in the future. By doing this, the company and developers can use funds from the sale of future tokens to develop the network or technology required to create a functional product and token and then deliver these tokens to investors who expect a liquid market where they are able to sell these tokens if they wish.

Some key features of a SAFT include:

- Tokens instead of equity: Blockchain companies who require a token as an integral part of their technology are now able to raise funds from venture capitalists in the same inexpensive and straightforward way that equity-only companies are able to.

- Accredited investors: SAFTs are typically offered to accredited investors who must complete KYC and AML checks. This is important because fundraising via a SAFT could be considered a security offering in certain jurisdictions and may be subject to regulatory oversight.

- Funding of product development: SAFTs are used to raise funds to develop the blockchain project. They provide a mechanism for early backers to invest in a project before the tokens are fully functional and tradable.

- Conversion Trigger: Similar to SAFEs, SAFTs include a trigger for the conversion of the investment into tokens. This trigger is typically based on the token contract being deployed and the tokens being generated, this is known as a token generation event. Tokens issued to early investors via a SAFT are generally subject to further illiquidity conditions or lock-ups, known as a cliff and then vested to the investor over a period of time specified in the SAFT. It is worth noting that it is common practice to include a contractual deadline in SAFTs that will state a maximum date in which the TGE will occur. It is best to be mindful that this date may mean you are contractually obligated to conduct your TGE before you would like to and can lead to a premature token launch in some cases.

- Risk: SAFTs carry risks for investors, similar to SAFEs, as they represent a promise of future value, and the success of a blockchain project is uncertain. A SAFT also only grants an investor an allocation of future tokens, if the blockchain project pivots their product and no longer requires a token to function, a SAFT investor does not have any equity claims against the company.

SAFE+T

The SAFE+T or Simple Agreement for Future Equity + Token (side letter or warrant) is a new fundraising instrument that has been adopted by startups building in the blockchain space who are looking to raise venture funds and may potentially release a token in the future. A token side letter or warrant are technically not the same but when written correctly they achieve the same outcome, for ease of explanation only the term side letter will be used going forward.

The token side letter component of the SAFE+T grants investors the option to receive future tokens, if they are issued, alongside or instead of the equity component of the blockchain company. There are many different ways to structure the equity to token allocation or conversion and are generally subject to negotiation with investors.

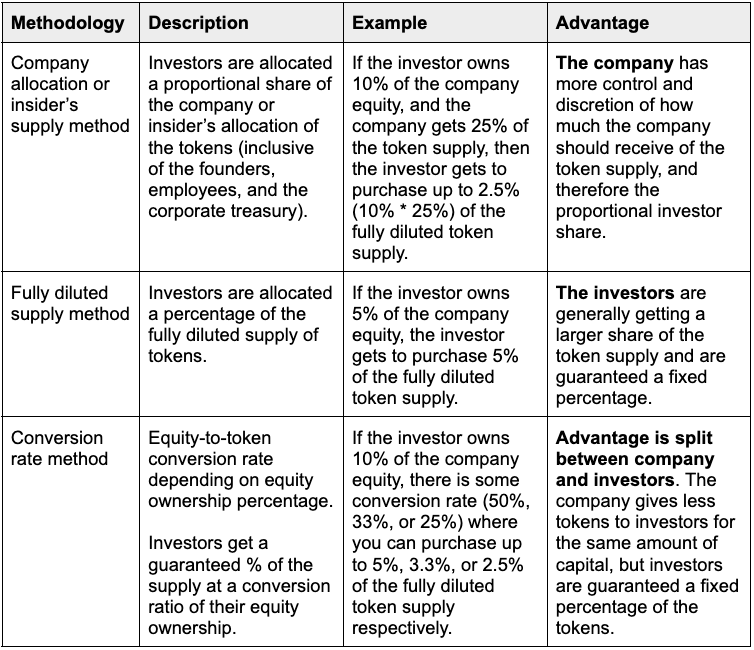

The three main ways of issuing tokens under a SAFE+T:

- Pro-rata allocation based on equity ownership with the founder pool allocation

- Pro-rata allocation based on equity ownership from fully diluted token supply

- Allocation based on fixed rate conversion from equity to token e.g. 4:1 conversion rate, 10% equity warrants 2.5% token allocation

Note: Side letters do not always include the right to allocation. Some side letters may be structured as right to purchase at given economic terms. While some other agreements may be structured by giving the shareholder choice between converting into both equity and tokens, and yet in others, token allocation is in lieu of equity.

Source: Crypto Fundraising with Token Side Letters or Token Warrants

Each of these options have their own advantages and disadvantages for the company and investors. It is imperative that when you are structuring your fundraising documentation you understand some fundamental things such as:

- Whether the value of your blockchain project is accruing in the token, equity or both;

- What a suitable valuation is for your tokens and equity, both individually and combined; and

- How much leverage do you have over the investors; Is the demand to invest higher than the amount of funds you want to raise?

It is important to ensure that you are clear on the above points with the investors so that you don’t end up with the wrong token side letter terms, or delay closing the deal because of misalignment on valuations.

Deciding which instrument to use

When determining which fundraising instrument to use it is important to ensure that the thought process is originating from a product perspective, rather than deciding if you want a token or not and trying to shape your product around that. Many teams opt for token models because of the go-to-market network effects with the business model being a secondary consideration. This may not lead to successful fundraising as investors will be seeking clarity around why a token is needed, its utility and whether it captures value as the product or service grows.

Value accrual must be carefully considered when crafting a business model. For example, does value accrue to the equity component of the company, the token component, or both?

To dive deeper into the decision between having a token or not having a token, refer to Outlier Ventures article ‘Does your product need a token?’.

Key questions to consider if you’re thinking about raising via SAFE, SAFT or SAFE+T:

- Does your product benefit from a token?

- Do you plan to launch a token with the product or at a later date?

- Where does the value accrue?

- Can the product or service be successful without a token?

- What is the monetisation strategy of the product or service?

If yes to a token:

- What is the utility of the token?

- How does the token capture value as the product scales?

- How will the token be distributed to stakeholders?

Recently there has been a move away from SAFT contracts with founders and investors favoring SAFE+T as it gives both the investor and the company raising extra protections in terms of deadlines to launch a token and freedom for future product pivots that may cause a change to some of the considerations above.

Some key learnings over Outlier Ventures’ 250 portfolio experience:

- Fundraising with tokens has more success in bull markets, but becomes less popular in market downturns among investors. Keep this in mind when discussing which fundraising instrument you will use with investors and don’t get forced into an unsuitable contract just to close the deal.

- SAFE+T gives founders more flexibility in regards to when a token is launched. We have seen companies contractually obligated to launch their tokens during unfavorable market conditions due to their SAFT conditions.

- If using a SAFE+T it is important to clearly define whether the value accrues to equity or token. If it accrues to both, you will need to negotiate the conversion of token to equity and the valuation for both the equity and token components.

- If not much thought has been put into a token it is best to raise via a SAFE and discuss a token with investors in the future if it arises. Investors expect to know details around token utility and value capture if you introduce a token side letter.

- When raising on a SAFE+T or SAFT it is important to have a thought out token design which you feel comfortable pitching to investors, along with detailed token allocations and vesting terms. The token is the vehicle investors will have exposure to, especially in the case of a SAFT, so it is important they know the details have been thoroughly thought through.

Conclusion

Hopefully this high level guide has given an increased understanding into the three main options founders have when looking to fundraise for their Web3 startup. Unfortunately there are many nuances with this thought process, especially if you decide to use the SAFE+T option and value accrues to both the equity and token components to varying degrees. This is why it is always important to consult seasoned professionals in the space who have advised a variety of blockchain based startups over the years on their business structure and fundraising.

Outlier Ventures Basecamp is a 12 week accelerator program that offers startups access to our Token Economies, Fundraising and Legal teams that can bring their wealth of knowledge to the table to answer any questions you may have and guide you regarding tokens, fundraising and entity structure.