Peer-to-peer electronic financial instruments

Bitcoin is a peer-to-peer electronic cash system. DeFi is a peer-to-peer electronic financial instrument system and refers to projects that are using cryptographic tokens and blockchains enabling anyone to issue, transfer and own financial instruments. The maturity of the Ethereum network has resulted in a slew of projects that are issuing not just ERC20 tokens but all types of financial instruments. Bitcoin emerged as an alternative to the financial system but the lack of features (which is a feature in itself) – has made it difficult to create complex financial instruments on it. But the smart contract functionality on Ethereum led to the relatively easy creation of complex financial instruments. While the Lightning Network does open Bitcoin up to micropayment use cases, realistically it is unsuitable for the sorts of instruments that can be created using full smart contract functionality. Other networks like EOS, Cardano, Dfinity, and lots of others with smart contract functionality could potentially be used by DeFi projects, but for now, Ethereum is the market leader predominantly because it has the largest developer mindshare and lots of ETH holders looking to put their money to work.

It is important to note that open-finance and decentralised finance are two different terms that may converge at some point and share similar attributes. Open finance points towards an unbundling of banking services where API-enabled startups provide niche services in a limited geographical region. They require full AML/KYC and are often B2C focused. Decentralised finance on the other hand often runs pseudo-anonymous, could potentially be censorship resistant, caters to a global market, and is considerably more transparent thanks to their operations running on public permissionless blockchains. When a decentralised exchange is hacked, it shows on a verifiable, public ledger. Decentralised finance could theoretically cater to the global market in comparison to open-finance projects that require routine license renewal and compliance with the legal policies of each region. Of course, as with almost everything in crypto-land, this is all still very much a legal gray area.

What is Decentralised Finance or DeFi?

In order to fall under our definition of “decentralised finance” a project would be required to have the following attributes:

- Censorship Resistance – Token custody, transfer, and exchange cannot be restricted by a handful of players responsible for maintenance of the network.

- Programmable Assets- Assets that are handled on the product should have all the native attributes of conventional tokens on a decentralised network.

- Pseudonymity – Decentralised financial applications should be able to leverage web 3.0 standards for signing of transactions and authentication. Thereby, drastically reducing the need for AML/KYC and making financial tools inclusive to a broader audience.

- Transparent and trustless – The current custodian of an asset in a de-fi project should always be verifiable on the blockchain and its custody should only involve smart contracts and wallets. There should not be large, centralised, exchange owned wallets in a de-fi product. In the presence of a smart contract, the code for the same should be open-sourced.

- Permissionless – Unlike “open-finance”, decentralised finance should allow anyone to create applications without the need for applications being approved by large, central banking authorities.

Keeping these in mind – one could define a decentralised finance application as a censorship-resistant, transparent tool that enables the transfer, custody, and exchange of tokenised assets that may be fungible or non-fungible in a permissionless environment with almost no requirements for identity verification. Decentralised finance varies from “open-finance” in the conventional sense because much of the stack in “open-finance” relies heavily on traditional banking entities that require strong AML/KYC requirements and fall largely under the regulatory purview of government bodies.

These lines have blurred to a certain extent for the purpose of creating the market-map. A dollar pegged token with central custody like Tether cannot be truly considered “decentralised finance”, however, it plays a major role in the ecosystem currently. Similarly, Nexo is a relatively centralised lending entity when compared to an alternative like Dharma Plex. However, in terms of liquidity and token offerings, the platform offers the highest and has therefore been included. Projects that require a heavy amount of AML/KYC or work directly under the purview of banks (Eg: JP Morgan’s Interbank Information Network) have been excluded as they are not as inclusive as Bitcoin is. The line blurs a little more when it comes to securities offerings due to the heavy regulatory requirements involved. Much like how decentralisation itself is a spectrum, decentralised finance has projects that range from complete inclusion to ones with certain entry barriers. With this in mind, it is to be noted that not all the projects mentioned in the market-map may be ‘decentralised’. They are however a gradual step towards creating a more inclusive, transparent and efficient financial ecosystems.

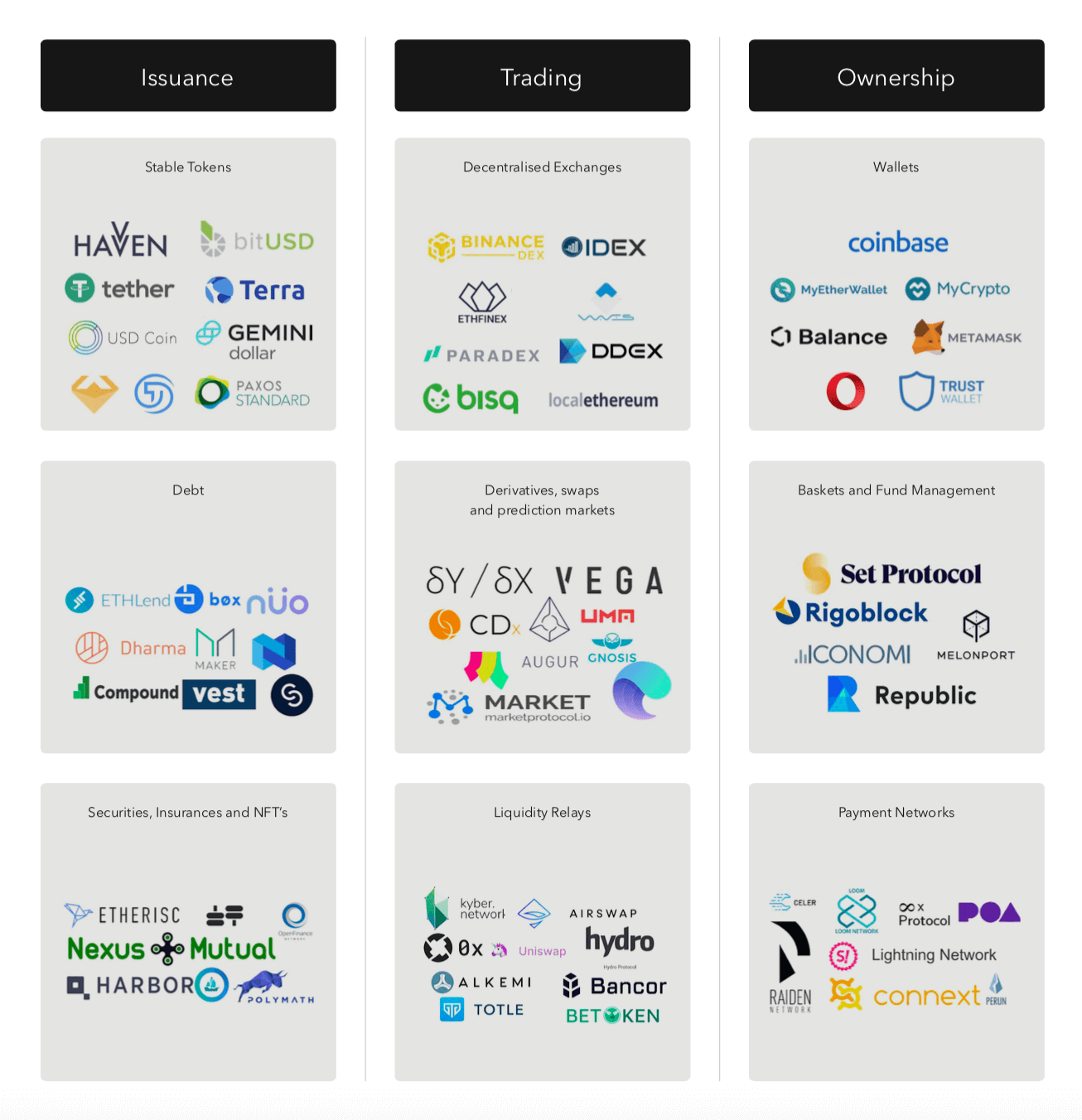

The single largest use-case within the De-Fi ecosystem currently has been for stable tokens. Within these, Dai tends to own the vast majority of the market if we discount tether due to its centralised nature. There are a number of other, associated products that have emerged as a result of the same. We broadly categorise them across issuance, trading, and ownership.

- Issuance

Broadly, issuance here refers to the creation of a new asset (eg: tokenised debt) that can then be traded, transferred or used as per requirements. In an ideal world, there should be little barriers to issuance (eg: ERC-20 tokens on Ethereum) and details regarding its issue, supply and transfer should be publicly verifiable. ICO tokens are one instance where issuance has become a prominent trend.

- Trading

Trading in this context involves infrastructure that enables the trading of assets that are tokenised. Niche token instruments such as derivatives or prediction markets that are native to stand alone platforms (eg: Numerai Erasure, CDx swaps) will be considered under trading instead of issuance since these assets are native to the platform they are traded on.

- Ownership

Ownership in our definition would refer to solutions that enable the custody of a token asset or its growth through lending based products. A product that allows loan issuance could belong to both issuance and ownership depending on who the user is. For the individual taking the loan, it would be an issuance platform. For the individual offering non custodial lending (eg: Dharma Protocol), it would be categorised under ownership since the product is a mechanism to increase token holdings without centralised custody. Similar to a bank’s fixed deposit offering that offers an annualised interest rate on deposits.

1. Issuance

While tokenizing of physical assets (eg; REITs on a blockchain) has been a key focus area over the past 2 quarters, current trends indicate that demand primarily stems from creation of virtual assets that can be traded. The cryptokitties phenomenon of 2017 was a run-up to the heightened interest in issuance of new virtual assets that derive demand from market perception of a virtual asset. We will see stable tokens continue to dominate under “issuance” with a clear power law evident as Tether and Dai take the lead. It is also likely that with Facebook and Coinbase likely to enter the remittance space, issuance of digital assets backed by fiat currency becomes a core focus area for the industry in the quarters to come. A resurgence of MobWars or Farmville (remember those?) like social games with NFT tokens is not unlikely. These would contribute substantially towards individuals opening up to virtual assets more and give existing, ad-driven businesses an alternative business model to explore.

1.1 Stable Tokens

Within the constraints of the definition of decentralised finance given above, it is safe to suggest that algorithmic stable tokens that do not require a centralised, banking entity are the only tokens that are truly “decentralised”. Any requirement for asset, commodity or fiat backing could bring a great element of decentralisation in the process. If a stable token’s issuer (eg: USDC) can dictate the terms upon which a dollar redemption is made, it is not safe to suggest that it is decentralised. Although ERC-20 tokens that are backed by Fiat can be used for the purpose of creating De-Fi applications, the centralised nature of the custody of the assets backing those currencies, make it highly risky. With Basis being shut down abruptly, MakerDai has been able to capture the bulk of the markets. Most decentralised exchanges and de-fi oriented products in the market are built on Dai. In the future, we’ll see two broad streams of stable tokens emerging. One will be lead by exchange collaborations (eg: Terra). The primary intent of these tokens will be to provide a stable alternative to traders and a hedge against banking services being cut off. Digitally native stable tokens will also contribute towards cutting off middle-men in internet run businesses that lose heavy margins to banks and foreign exchange rates. Subscription layers to enable these payments are already being created by the likes of Groundhog. We may also see competition between social networks such as Facebook and vKontact to create regional stable tokens to enable on-platform shopping experiences. Instagram’s move towards enabling users to purchase from the platform is an early move towards this.

1.2 Debt Markets

The competition here is in terms of interest rates offered and liquidity provided. Since the market is still in its early stages, traders and lenders choose to go with platforms that offer the highest amount in interest. Interest rate settlements may be in tokens (eg: Eth) or in dollar terms. Platforms like Compound and Dharma currently offer token settled interest rates. This is hugely attractive to token holders with large sums that wish to grow their token amounts with little risk. The rise of staking platforms have added a new layer of complexity to debt markets. It is likely that we see entrepreneurs arbitrage between debt markets (take token denominated debt for the low amount in interest) and arbitrage with staking interest received. Staking specialists like Vest and Staked will provide custodian services and offer interest at the same time and will thus compete against debt markets for market-share. Over the course of time, market efficiency will lead to a convergence of staking and debt based returns in token terms. Token-based debt markets also hold the power to bring together markets with variations in regional interest rates. Nuo.network, for instance, is seeing a high degree of interest from Japan where the inflation rate stood as low as 0.2. Given the pace at which tokens can move globally, it is likely that investors move currencies from low inflation rate markets to tokens and loan them out for higher interest offerings when compared to what their banks offer. There has been an attempt at creating a standard inter-platform token lending rate in the form of DIPOR by The Block.

1.3 Securities, Insurance and NFTs

Insurance in De-Fi is likely to not take off until IoT enabled verification or better forms of oracles come of age. Currently, most of the traction is captured within Harbor and Polymath through ongoing collaborations with platforms like Smart Valor. Security tokens will rely heavily on regional regulations giving a thumbs up before we see them capture substantial traction. Abacus and Open Finance network fair better than competitors due to their relatively advantageous positions from a regulatory angle. NFTs are yet to come of age. With gaming platforms built with blockchains evolving and AR/VR applications emerging, we may see NFTs being a core component of the ecosystem. For now, the bulk of the value for financial applications remain within securities. It could also be argued that this segment of De-Fi has a relatively high degree of centralisation due to its reliance on a central entity for issuance. Changes in governance structures for STOs will combine the advantages of regional regulatory oversight, on-chain governance and decentralised ownership. However, this will rely on the pace at which regulators move. France, Switzerland and Singapore lead in terms of clarity for the moment.

2. Ownership

Between India’s demonetisation drive in 2016 and Venezuela’s current monetary situation, it is fair to suggest that private ownership of stores of value with instant redemption will be crucial to citizens going forward. Given the number of times exchanges have been hacked, the market may have an appetite for products that enable financial services without losing custody. It could involve tracking the price of a basket of coins (eg: Set Protocol), making direct peer to peer payments with no middle men (eg: xDai, Local Ethereum) or independent storage. Broadly, we categorise them as wallets, fund management and payment networks.

2.1 Wallets

Currently, Metamask is the preferred web 3.0 wallet. The ease with which it integrates with browsers makes it a preferred solution for DeFi users. MyEtherWallet has relative dominance due to their integrations with hardware wallets (ie – ledger, trezor). A new crop of wallets like Balance and Trust emphasise heavily on user experience as a moat. However, the lack of browser integration would mean, it is likely that Metamask maintains dominance in terms of number of wallets until mobile app based de-fi products come of age. In addition, the emergence of in-browser wallets like those offered by Opera and Brave browser will bring millions of new users who had previously never heard of tokens to the ecosystem. These wallets will contribute substantially towards an increase in usage of NFTs (non fungible tokens) in consumer applications like games. It won’t be long before we see in-game assets traded through browser based wallets.

2.2 Fund Management

ICONOMI has been a leader in terms of volume attracted for fund managers to set up open, trackable portfolios. However, the project is largely centralised. A prominent competitor that works in a decentralised fashion currently is Rigoblock. The startup has an on-going collaboration with Ethfinex wherein individuals can trade on Ethfinex and show a public portfolio listed on rigoblock. The set protocol offers a similar approach of creating baskets of tokens and allowing individuals to buy them. Another key player in the decentralised fund management space is Melon Protocol. The protocol allows managers to set up their own customized rule-sets for an on-chain hedge fund, basket, tracker or ETF which interacts with tokens and enables anyone with tokens to invest. The rulesets are enforced by the smart-contracts.

Most centralised funds have little, verifiable proof of holdings, performance, fees & risk management. Melon protocol offers a single dashboard that allows individuals to verify all these characteristics and more — the dashboard is backed by on-chain smart contract proofs and enables investors to self-custody their assets rather than having to trust a 3rd party. Social trading may likely not take off until the next bull cycle enters the market and individuals need tools like trading view to share their portfolio’s performances. The next bull cycle will also witness “social trading” elements that connect to an individual’s wallet for portfolio tracking and identity.

Settle.finance is an early example.

2.3 Payments Networks

There is a small crop of startups emphasising specifically on improving the pace at which payments occur. xDai is a project on POA network that offers Dai’s stability and web 2.0 speed. Similarly, Matic network claims instantaneous payments although with a very high level of centralisation. Emergent payment networks are too early stage to define a clear winner yet. Payment networks in De-Fi will likely need a service like Stripe that allows individuals to pay with conventional means on one end (eg: credit card) and offer tokens on the other end (eg: Dai). This comes with a high degree of risks associated with fraud and forex slippages but it has the power to improve the revenues of digital first internet companies. As payment networks come of age, token based escrow systems will also lead to the creation of new age business models that were previously not possible.

3. Trading

One element about trading in the defi-ecosystem that differentiates it from mainstream finance is the barriers to wash-trading within it currently. Fees associated with relaying exchange requests (eg: Gas expenditure on IDEX orders) could make it relatively more difficult to spoof orders and manipulate markets. However, this comes with the great disadvantage of slower order settlement and possibly, thinner books. Ethfinex had a market volume of 95 million for Eth tokens alone, followed by Omisego which had a paltry volume of 2 million in comparison. Market-liquidity and arbitrage in Decentralised ecosystems is still picking up and it will likely take time before we see market-efficiency in token prices like we do with centralised exchanges. Scaling solutions will play a key role in making this transition occur. Much like how traditional finance underwent a period of digitisation in the 1980s, we’ll witness a move to decentralise trading avenues, bringing markets closer, reducing trade barriers and a surge in transparency on how markets function. Where traditional banking is seeing an “unbundling” process, protocols are beginning to evolve to provide complete banking services on their own. The ideal scenario being one where an individual can trade, loan and hold tokens on a single platform. MarketProtocol has been contributing substantially towards making this happen.

3.1 Decentralised Exchanges (Dex)

The key reason why decentralised exchanges appeal to an increasingly larger audience is the elements of instantaneous custody and no withdrawal limits. Traders that have had painful experiences with MtGox hacks and long hours of waiting while exchanges verify their AML/KYC documents would rather prefer to trade on a decentralised exchange than go through a centralised alternative. They would also be preferred in regions with strict controls on trading. With the emergence of stable tokens like USDC, DAI and USDT, traders would prefer to book their capital gains in stable assets and convert to cash through P2P mechanisms and avoid reporting to the government altogether. Another aspect we’ll see through Dex’s will be an emergence in currency conversions without government involvement. Peer to peer mechanisms involving cash could be used to convert money to Ether and then a decentralised exchange could be used to purchase a stable dollar pegged token. Local Ethereum’s integration of Dai points to a possibility of this occurring. In regions like India, where inflation is as high as 6%-7%, this will be a route to circumvent government limits on conversions to dollar. Dex liquidity and UX however remain woeful currently. The leaders in fixing this challenge currently remains centralised exchanges that launch “trustless”variants of their own operations. Binance and Bitfinex have their own decentralised exchange offerings. There’s also concerns around front-running in decentralised exchanges emerging.

3.2 Derivatives, Swaps and Prediction Markets

We are still at the earliest stages of seeing this element in trading take off. DyDx and CdxProject are currently in the inception stages of their products going live. DyDx allows individual investors to purchase margin long and margin short tokens whilst CDX enables the creation of credit default swaps that allow traders to hedge against an exchange being hacked. Nuo has a functional, non custodial margin trading platform that uses reserves loaned out by other users to help individuals trade on leverage. Prediction markets like Augur and Gnosis currently suffer from UX challenges and user-awareness. While projects like Veil and Guesser are attempting to make these tools easier to use they still have a long way to go. Numeraire’s move to enabling individuals to create prediction markets of all kinds could prove to be ground-breaking due to their current community of data-scientists.

3.3 Liquidity Relays

Although decentralised exchanges remove the need to trust a central entity with custody of tokens (barring smart contract transfers), challenges in liquidity still plague them. Tokens could be selling at variable prices in different exchanges and may not have the necessary amount of liquidity needed to handle large orders. One way the De-Fi ecosystem mitigates this is through liquidity protocols like 0x and more recently, tools like Totle. Totle’s app currently allows individuals to create a basket order of multiple tokens and relay them across a large number of exchanges with a handful of clicks. Orders for tokens are settled in different exchanges and the new erc-20 token is transferred back to the user. The use of metamask for signing transactions makes the complex process of engaging with multiple exchanges far more intuitive. An outlier among these is Uniswap. The project is an automated market-maker with reserves that pay a small fee (.3%) of the trade involved. With interoperability protocols like Cosmos and Polkadot coming of age, it won’t be long before cross-chain dex transactions become common. Between tokens tied up in centralised exchanges, personal custody and reserves in decentralised exchanges, there will be a gap for a protocol layer that enables arbitrage between lending, trading and where ideal, even staking. Kyber’s integration in MyEtherWallet to provide in-wallet exchanges is an example of how liquidity relays contribute monumentally towards improving customer experiences.

The Future

Individual users won’t want to use multiple platforms for their transactions. Users will largely converge around on-ramps (eg: exchanges) and wallets (eg: balance.io). Given the open-source and decentralized nature of these projects, each of them will be able to interconnect with one another to enable trading, storage of existing assets, insurance and the like within the same platform. We are seeing some early variants of this with Trust Wallet offering interactions with Dapps. Platforms like Morpher.io and Abra are beginning to combine traditional instruments like equity with tokens and it will play a major role in driving individuals in remote parts of the world to have exposure to previously unattainable foreign assets. Over time, De-Fi platforms may remove the complexity added by regulators in the interest of keeping economies walled away and allow retail investors without the necessary tools (eg: specialist banks) to get access to commodities, exotic assets, derivatives, foreign currencies, and even equity.

The DeFi ecosystem, in its entirety, is perhaps worth around ~$1 billion. Today, the bulk of this comes from MakerDAO. Considering the total market-capitalisation of $173 billion, it is worth less than 1% of the total ecosystem if we take token market capitalization as a proxy. However, decentralised finance is one of the few instances where a tokenised product is used routinely. It has the power to bring the “utility” back to utility tokens. Decentralised finance has the power to enable applications that were considered possible in 2013 but difficult to pursue due to scaling challenges and volatility. The emergence of stable tokens, payment systems and lending platforms could make opportunities for entrepreneurs around the globe and bring our financial markets closer while increasing transparency. While there is a great systemic risk in these systems (eg: Dai locked up with eth, used to buy Eth), they offer an alternative from the banks who with their CDOs may have put an entire generation to peril in 2008. It is too early to suggest any of them are clear winners. However, it may be just as early to suggest DeFi will not bring value to the ecosystem.

400 years back, when entrepreneurs traveling far and wide in search of new opportunities issued stock, it was a mechanism for individuals to share the risks and rewards of new ventures. It democratised access to the means of wealth generation. 10 years back, when Satoshi released Bitcoin’s code, he created a financial system that ensured the sovereignty of an individual’s wealth remained with them.

Decentralised finance is a gradual evolution of the same. It holds the power to bring our markets closer than ever before, eradicate unnecessary middle-men, bring considerable cost efficiencies and opens access to communities that have until now remained under-served. Much like the web, it will initially cater to a privileged few, but its benefits will pass on to an entire generation of under-served consumers who may never had access to loans or the means to make payments abroad. If macrotrends like the gig economy and globalisation are to continue going forward, the financial infrastructure to enable that needs to fall in place.

With decentralised finance, we have our first true shot at making it happen. When Satoshi released Bitcoin’s whitepaper, it came at a time when banks were at the brink of yet another bailout. Decentralised finance, builds upon his vision, of giving individuals dignity, sovereignty, and transparency about how their hard-earned assets are stored and invested. It isn’t the antibanking establishment. It is a pro-consumer choice. And in building it, one isn’t derailing the power of the government or banks, but rather empowering the common man to have an alternative in an ecosystem where there hasn’t been one for centuries.

Engage with us

Our reputation has originated as a consequence of our deep commitment to open research and thought leadership in the decentralisation space broadly, and more specifically, through our Convergence Stack thesis.

We engage regularly with start-ups, academia, and the corporate ecosystem and are open to collaboration and consulting opportunities throughout the community. Current research themes are focused on smart cities, energy, mobility, connectivity, augmented reality, and “crossing the chasm” to mainstream decentralised technology adoption.

If you wish to discuss your project or initiative further, please contact Lawrence, Charlotte or Catherine.

Download the full report here: Mapping Decentralised Finance (DeFi) report

DISCLAIMER

This email is intended only for the person to whom it is addressed. No one else may place any reliance upon, copy or forward all or any form of this email in any way. If an addressing or transmission error has misdirected this email, please notify the sender by responding directly, ensure the email is deleted and is not used, disclosed, copied, printed or relied upon in any manner. To the extent permitted by law, Lawson Conner Services Ltd does not accept or assume any liability, responsibility or duty of care for any use of, or reliance upon, this email by anyone, other than the intended recipient, to the extent agreed in the relevant contract for the matter to which this email relates (if any). Lawson Conner Services Ltd is a Company registered in England and Wales, registered number 07277134. Lawson Conner Services Ltd, Sapia Partners LLP and G10 Capital Limited are part of the Lawson Conner Group. Lawson Conner is part of IQ-EQ.